The United States is Leading the LNG Charge

Authored by Scott McKenna and Ed O’Toole.

It’s said that history doesn’t repeat itself, but it often rhymes. Such is the case with the US energy industry and specifically, US LPG and LNG exports.

|

Advertisement: The National Gas Company of Trinidad and Tobago Limited (NGC) NGC’s HSSE strategy is reflective and supportive of the organisational vision to become a leader in the global energy business. |

In the early 2000s, many energy experts believed that US energy production had seen its pinnacle and the country was destined to be an energy importer for as far as the eye could see. Lo and behold, the shale revolution dramatically changed everything, and by the early 20 teens, the US began to flip terminals around from imports to exports.

LPGs really led the way as propane and normal butane began to flow out of US terminals (the U.S. become a net exporter in 20121) to feed what would become an almost insatiable appetite for MMBtus. The US is now the largest global LPG supplier with export capabilities exceeding 75% of total domestic production. That’s no slouch to say the least!

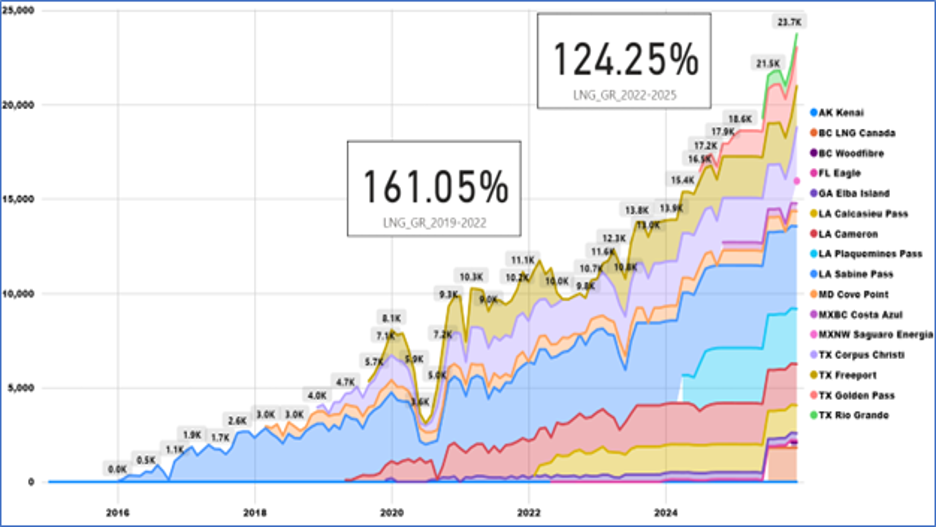

Not long after, US LNG terminals flipped their switch, import terminals reversed flow capabilities and started down a very similar path becoming a net exporter in 2017.2 Unsurprisingly, the US Gulf Coast is the primary source of export capacity, having a favored proximity to the prolific Permian and Haynesville basins. Not to be outdone, however, is the robust Appalachian basin featuring the Marcellus shale play, which has dramatically altered historical pipeline flows. This basin not only supplies local export capacity, at the likes of Cove Point LNG in Maryland, but also the same Gulf Coast terminals served by the Permian and Haynesville.

RBAC, Inc. is the market leading supplier of global and regional gas and LNG market simulation systems. The G2M2® Market Simulator for Global Gas and LNG™ is designed for developing scenarios for the converging global gas market. It is a complete system of interrelated models for forecasting natural gas and LNG production, transportation, storage, and deliveries across global gas markets. For more information, please visit our website at http://rbac.com.